Discover how to choose the right Document Management System (DMS) for enterprises in Latin America, focusing on regulatory compliance & cloud...

How Banks in Latin America Ensure Compliant Customer Communications. Learn how automated workflows and CCM platforms help banks navigate complex regulations.

Latin American banks are digitizing at an unprecedented pace, but fragmented regulatory frameworks across Brazil, Mexico, Colombia, Chile, Peru, and Argentina create significant compliance risk in every customer-facing document. A single non-compliant statement, an inaccessible contract, or a missing audit trail can trigger fines, litigation, and lasting reputational damage. The tension is real: rapid digital transformation is accelerating the volume and variety of outbound communications, while regulations governing those communications continue to evolve independently in each jurisdiction.

Outbound documents, including statements, notices, contracts, alerts, and onboarding materials, are among the most common failure points in banking compliance programs. They sit at the intersection of data privacy, consumer protection, and accessibility obligations, and they must function correctly across print, email, SMS, WhatsApp, and app-based channels. This guide walks through the regulations that apply, the risks banks face, and how automated document workflows, particularly Customer Communications Management (CCM) platforms, close the compliance gap across every channel and jurisdiction.

Quick Summary

Regulatory compliance in banking customer communications means every outbound document must meet jurisdiction-specific rules on data protection, transparency, language, format, and accessibility. In Latin America, fragmented and fast-evolving regulations across Brazil, Mexico, Colombia, Chile, Peru, and Argentina make compliance especially challenging. Automating document generation, delivery, and audit logging through a CCM platform reduces human error, enforces rules at scale, and ensures banks maintain a defensible compliance posture across all channels and jurisdictions.

What Does Regulatory Compliance Mean for Banking Customer Communications?

Regulatory compliance in banking customer communications requires every outbound document, from account statements to loan disclosures, to meet jurisdiction-specific rules on data protection, transparency, language, format, and accessibility. This is not a general IT compliance concern; it is a distinct operational discipline.

In a banking context, "customer communications" encompasses a wide range of document types: account statements, transaction alerts, loan and credit disclosures, contractual agreements, onboarding packages, regulatory notices, marketing messages, and digital notifications. Each of these must comply with applicable regulations at the moment it is generated, delivered, and stored.

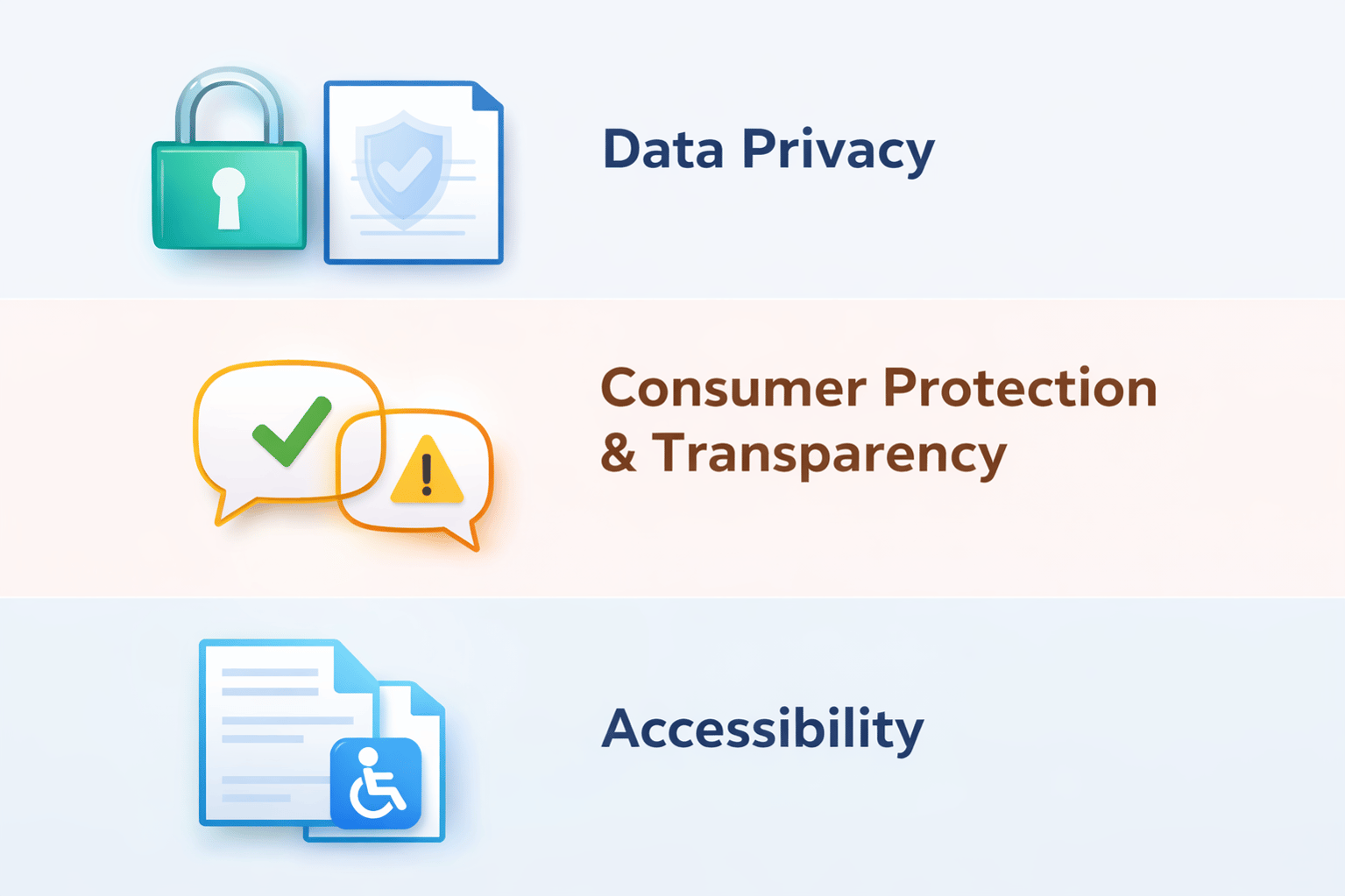

Compliance obligations across Latin America cluster around three foundational pillars:

Data privacy. Laws such as Brazil's LGPD and Colombia's Habeas Data Law require banks to establish a legal basis for every communication, minimize the personal data included, and support data subject rights such as access, correction, and deletion.

Consumer protection and transparency. Financial regulators such as Mexico's CNBV and Colombia's Superintendencia Financiera mandate clear, complete, and understandable disclosures. Banks must present terms, fees, and conditions in plain language and in formats accessible to the intended audience.

Accessibility. Document accessibility, including compliance with PDF/UA standards, is shifting from best practice to regulatory expectation, driven by the European Accessibility Act (EAA) and emerging LATAM inclusion requirements. As of June 28, 2025, the EAA requires businesses operating in or serving EU markets to ensure their digital content, including PDFs, is accessible to people with disabilities.

These three pillars apply to every communication a bank produces, making customer communications management a critical compliance function rather than a back-office utility.

Which Regulations Apply to Customer Communications in Latin America?

Banks operating across Latin America must comply with a patchwork of country-specific data protection, financial supervision, and consumer rights laws. Key regulatory anchors include Brazil's LGPD, Mexico's Fintech Law and CNBV rules, Colombia's Habeas Data Law, Chile's CMF requirements, Peru's SBS regulations, and Argentina's data protection and BCRA cybersecurity expectations.

The table below summarizes the primary regulations affecting customer communications in each major LATAM banking market:

|

Country |

Key Regulation(s) |

Regulator(s) |

Scope Relevant to Communications |

Penalty Range |

|

Brazil |

LGPD (Law 13,709/2018); BCB Resolutions; Open Finance rules |

ANPD, Central Bank of Brazil |

Data consent for all communications; breach notification; document retention |

Up to 2% of revenue per infraction, capped at BRL 50 million (~USD 10.5 million) per violation |

|

Mexico |

Federal Data Protection Law; Fintech Law; CNBV regulations |

CNBV, INAI |

Fraud prevention plans; individual transaction limits; customer authentication |

Varies by regulation; CNBV can revoke licenses |

|

Colombia |

Habeas Data Law (1581/2012); Superintendencia Financiera guidelines |

Superintendencia Financiera, SIC |

Customer data access rights; algorithmic decision transparency |

Fines up to 2,000 minimum wages |

|

Chile |

Data Protection Law (reform in progress); CMF authentication rules |

CMF |

Strict customer authentication; refund/chargeback documentation |

Regulatory sanctions; pending reform may increase penalties |

|

Peru |

SBS Regulation No. 2286-2024 |

SBS |

Two-factor authentication for card transactions; secure communications |

Administrative sanctions |

|

Argentina |

Personal Data Protection Law 25,326; BCRA cybersecurity rules |

AAIP, BCRA |

Data localization considerations; cybersecurity requirements for communications |

Fines per AAIP schedule |

International standards also shape local enforcement. The GDPR's influence is visible in Brazil's LGPD framework, while Basel frameworks inform supervisory expectations around operational risk and data governance across the region. There is a general trend toward harmonization, with countries increasingly referencing each other's frameworks and aligning with global data protection principles. However, the current reality remains fragmented: each jurisdiction enforces its own timelines, penalties, and interpretive guidance, making it essential for multi-country banks to manage compliance at a granular, per-market level.

Banks that operate across these jurisdictions benefit from centralized integration capabilities that connect document generation systems with local regulatory requirements without rebuilding workflows for each country.

What Are the Biggest Compliance Risks in Banking Document Workflows?

The five most common compliance risks in banking document workflows are sending communications without proper data consent, failing to meet accessibility standards, inconsistent document versioning, missing audit trails, and delayed breach notifications. Each of these can trigger regulatory penalties and compound across multi-country operations.

1. Sending communications without proper data consent. Banks must establish a valid legal basis before generating and distributing any customer-facing document. In 2024, the financial and insurance sectors were the most targeted by cyberattacks in Latin America, accounting for 33% of cases, according to the IBM X-Force 2025 report, underscoring how sensitive customer data in banking communications has become a high-value target. A communication sent without a valid legal basis can result in fines, mandatory data deletion, and processing bans.

2. Failing to meet accessibility standards. Documents that are not accessible to people with disabilities expose banks to legal risk, especially those with European operations or clients subject to the EAA. An estimated 1.3 billion people, or 16% of the global population, experience significant disability. Inaccessible statements and contracts effectively exclude this population from receiving compliant service.

3. Inconsistent document versioning. When template updates are not synchronized across all countries and channels, outdated or non-compliant documents continue circulating. This "template drift" is particularly dangerous in multi-country operations where local teams may maintain their own versions of standard templates.

4. Missing audit trails. Regulators increasingly expect banks to produce a complete, timestamped record of every document generated, delivered, acknowledged, and stored. Without automated logging, banks struggle to demonstrate compliance during inspections. The Digi Americas Alliance, Duke University, and Recorded Future found in 2025 that Latin America remains among the least prepared regions for cyber incidents due to underinvestment in cybersecurity, a shortage of qualified professionals, and weak regulatory frameworks.

5. Delayed breach notifications. Brazil's ANPD Resolution No. 15, effective since April 2024, requires controllers to notify the authority and affected data subjects within three business days of confirming an incident that poses relevant risk. Banks without automated notification workflows risk missing these tight deadlines, which can compound penalties significantly.

These risks are magnified across multi-country operations, where template drift, uneven processes, and inconsistent logging create compounding exposure. Banks that have addressed these challenges through centralized compliance tooling can review their approaches in published success stories.

How Does Data Privacy Law (LGPD, Habeas Data) Affect Customer Statements and Notices?

Data privacy laws such as Brazil's LGPD and Colombia's Habeas Data require banks to establish a valid legal basis for every customer communication, minimize personal data included in documents, and enable data subject rights, including access, correction, and deletion, within the systems that generate and distribute those communications.

Brazil's LGPD defines ten legal bases for processing personal data, outlined in Articles 7 and 11 of Law 13,709/2018. For banking communications, three bases are most commonly applied:

Legitimate interest applies to communications that serve the bank's operational or commercial objectives, such as cross-selling notices or service updates, provided the processing does not override the data subject's fundamental rights.

Legal obligation covers communications required by law or regulation, such as mandatory disclosures, tax documents, and regulatory notices.

Contract performance applies to communications necessary to execute or manage an active contractual relationship, including account statements, payment confirmations, and loan updates.

The distinction between consent-based and non-consent legal bases matters for practical template design. Marketing messages typically require explicit consent, while transactional statements and regulatory notices rely on legal obligation or contract performance. Banks must design their document generation systems to apply the correct legal basis per document type and channel, and to record that basis for audit purposes.

In practical terms, a compliant bank statement minimizes exposed personal data (showing partial account numbers rather than full numbers, for example), includes only the data necessary for the stated purpose, and is generated from a system that can demonstrate the applicable legal basis. A non-compliant statement might expose unnecessary personal data, lack a documented legal basis, or be generated from a template that was not reviewed after the most recent regulatory update.

Data subject rights also affect document workflows directly. Under LGPD Articles 18 and 20, customers can request access to their data, correction of inaccurate records, deletion of unnecessary data, and, critically, review of automated decisions. Between 2023 and 2025, Brazil's ANPD issued fines totaling approximately BRL 98 million (~USD 20 million), targeting sectors including finance, healthcare, and AI-driven processing. Banks must ensure their document generation and storage systems can respond to these requests within legally mandated timeframes.

A CCM platform deployed as SaaS can enforce these data handling requirements at the point of document generation, applying legal-basis rules, data minimization controls, and audit logging automatically.

Why Is Document Accessibility Now a Compliance Requirement for Banks?

Document accessibility, including PDF/UA-compliant PDFs and accessible digital communications, has shifted from best practice to compliance expectation for banks, driven by the European Accessibility Act, ESG pressure, and emerging LATAM inclusion requirements. Because banks often cannot ask customers about disability status under privacy laws, accessible-by-default documents are the safest operational standard.

The European Accessibility Act (Directive 2019/882) became enforceable on June 28, 2025, requiring businesses operating in or serving the EU market to ensure their digital content, including PDF documents, is accessible to people with disabilities. This applies directly to customer-facing documents such as bank statements, contracts, invoices, and product disclosures. For LATAM banks with European operations, clients, or group policies, EAA compliance is now mandatory rather than aspirational.

There is also a significant privacy paradox at work. Under data protection frameworks like the LGPD and the GDPR, banks generally cannot ask customers whether they have a disability. This means banks cannot rely on disability disclosure to decide which documents need accessible formatting. The only operationally safe approach is to produce all documents in accessible formats by default.

The market opportunity is substantial. Research from Accenture in partnership with Disability:IN found that companies leading in disability inclusion achieved 1.6 times more revenue, 2.6 times more net income, and 2 times more economic profit compared to peers in the Disability Equality Index, reinforcing that accessibility is both a compliance requirement and a business driver.

In practical terms, an "accessible PDF" is one that complies with the PDF/UA standard (ISO 14289), which requires tagged content structures, alternative text for images, logical reading order, proper language markup, and compatibility with screen readers and other assistive technologies. Producing these at scale requires automation embedded directly in the document generation pipeline.

DocPath enables accessible PDF generation at scale through its no-code platform, allowing banks to integrate PDF/UA compliance into high-volume document production without requiring specialized technical knowledge for each template.

Need to make your banking communications both compliant and accessible? Contact DocPath to see how our platform generates accessible, regulation-ready documents at scale.

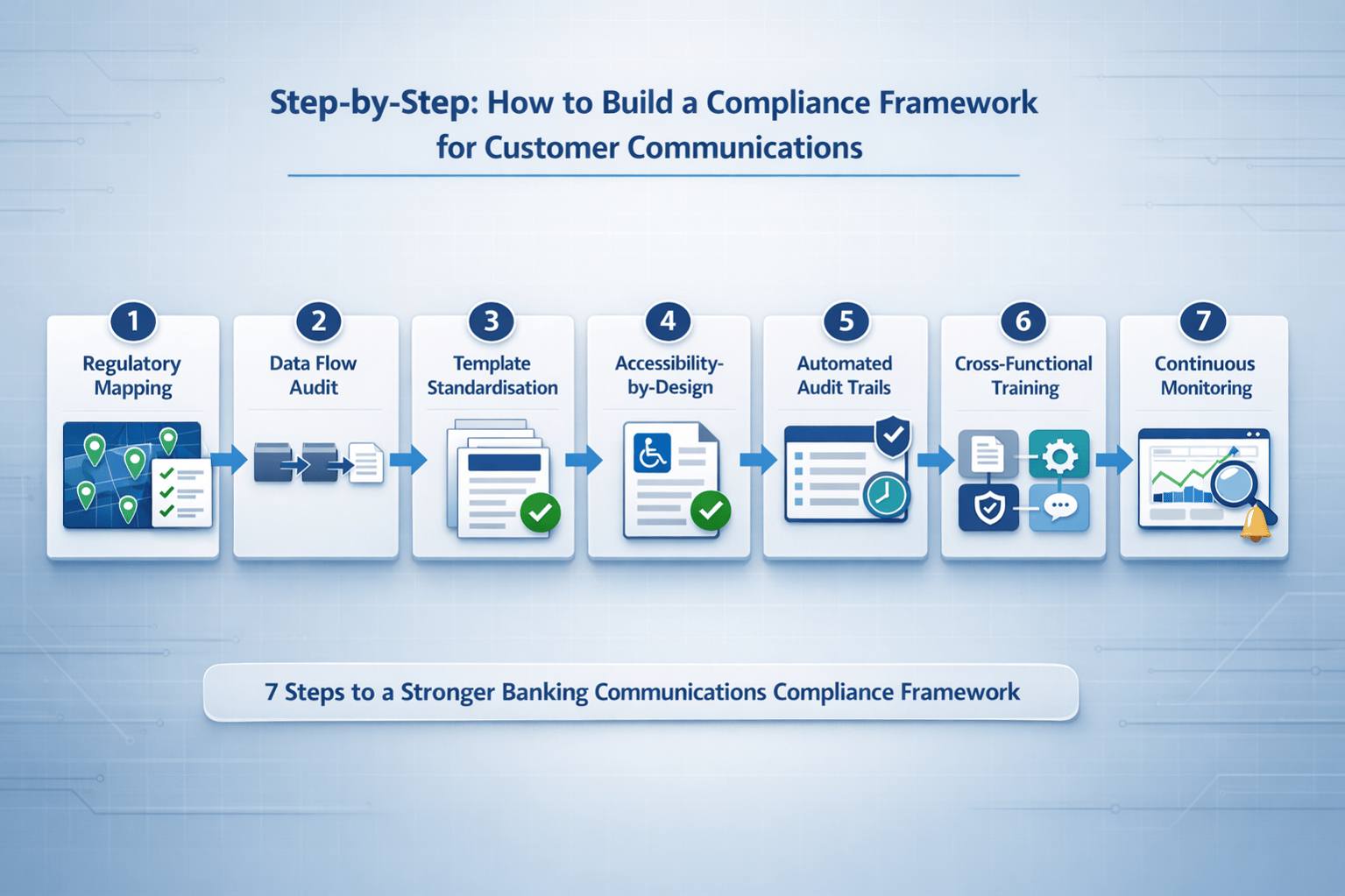

Step-by-Step: How to Build a Compliance Framework for Customer Communications

A compliance framework for banking customer communications requires seven steps: regulatory mapping, data flow audit, template standardization, accessibility-by-design, automated audit trails, cross-functional training, and continuous monitoring.

1. Map applicable regulations. Begin by identifying every jurisdiction in which the bank operates and cataloging the specific communications rules that apply in each. This includes data protection laws, financial supervisor requirements, consumer protection mandates, and accessibility obligations. The regulatory comparison table earlier in this article provides a starting framework for six major LATAM markets.

2. Audit your data flows. Trace how customer data enters, moves through, and exits the document pipeline. Identify every system that touches personal data during document generation, from core banking platforms and CRM systems to template engines and delivery channels. This audit should reveal gaps in consent tracking, data minimization, and retention practices.

3. Standardize document templates. Centralize template governance to enforce consistent compliance across channels and regions. A single source of truth for templates eliminates the template drift that occurs when local teams maintain their own versions. Centralized templates should include pre-approved regulatory language, data fields limited to what is legally required, and formatting that meets accessibility standards.

4. Integrate accessibility from design. Embed PDF/UA compliance and accessible formatting into the document design process from the start rather than retrofitting existing documents. This means building tagged structures, alt text, and logical reading order into templates before they enter production.

5. Automate audit trails. Configure systems to log every document generation event, delivery attempt, confirmation, timestamp, and acknowledgment automatically. Manual logging is error-prone and cannot scale across millions of communications. ISO 27001 guidance emphasizes that organizations must maintain records demonstrating the effectiveness of adopted security and compliance measures.

6. Train staff on compliance triggers. Marketing, legal, operations, and IT teams must all understand which communications trigger which obligations. A marketing email requires consent; a regulatory notice relies on legal obligation. Training should be ongoing and updated whenever regulations change.

7. Monitor and update continuously. Assign clear ownership for tracking regulatory updates in each jurisdiction and translating those updates into template and rule changes. In LATAM's fast-evolving regulatory environment, continuous monitoring is more effective than periodic reviews.

Banks evaluating how to implement these steps with existing infrastructure can explore DocPath's services for compliance framework design and migration support for transitioning from legacy document systems.

How Can a CCM Platform Automate Regulatory Compliance?

A Customer Communications Management (CCM) platform automates compliance by centralizing template governance, enforcing data handling rules at generation time, producing accessible output by default, logging document interactions for audit, and enabling multichannel delivery with jurisdiction-specific rules, all without requiring disruptive changes to existing ERP, CRM, or core banking systems.

For readers unfamiliar with the category, CCM refers to software that manages the design, generation, personalization, and delivery of customer-facing documents across all channels, including print, email, SMS, web, and app-based formats. In banking, CCM systems produce the statements, contracts, notices, and alerts that form the bulk of regulated customer communications.

The following table maps key compliance requirements to CCM capabilities and their business outcomes:

|

Compliance Requirement |

CCM Capability |

Business Outcome |

|

Consistent regulatory wording and formatting |

Template governance with version control |

Eliminates template drift and unauthorized modifications |

|

Data minimization and legal-basis enforcement |

Data extraction rules applied at generation time |

Ensures only necessary data appears in each document |

|

Accessibility compliance at scale |

Automated PDF/UA-compliant output |

Every document is accessible by default, meeting EAA and emerging LATAM requirements |

|

Audit readiness and traceability |

Automated audit logging of generation, delivery, and acknowledgment |

Complete, timestamped compliance evidence available on demand |

|

Channel-specific compliance with unified controls |

Multichannel delivery rules engine |

Consistent compliance enforcement across print, email, SMS, WhatsApp, and app channels |

DocPath's CCM platform offers no-code template design, a high-performance document generation engine (DGE) capable of millisecond-level output at very high volumes, and integration with any data platform, including core banking systems, CRMs, and ERPs. This contrasts with manual or legacy approaches that rely on spreadsheet-driven template control, fragmented delivery tools, and inconsistent logging across channels.

Banks evaluating CCM platforms for compliance automation can explore DocPath's full solutions portfolio for detailed capability descriptions.

What Are the Most Common Compliance Mistakes Banks Make with Customer Documents?

The most frequent compliance mistakes include using outdated templates after regulation changes, failing to log delivery confirmations, sending communications without valid legal basis, neglecting accessibility, and treating compliance as a one-time project instead of an ongoing discipline.

1. Using outdated templates after regulatory changes. What goes wrong: a regulation updates disclosure requirements, but the corresponding template is not revised before the next production run. Why it happens: multi-country operations create dozens of template variants, and manual change management cannot track them all. How to prevent it: centralized template governance with version control and mandatory review gates tied to regulatory update alerts.

2. Failing to log delivery confirmations. What goes wrong: a bank generates and distributes compliant documents but cannot prove delivery during an audit or dispute. Why it happens: delivery logging is handled inconsistently across channels, with email receipts tracked but print and SMS confirmations ignored. How to prevent it: automated end-to-end audit logging across all channels, with timestamps and delivery status captured at each stage.

3. Sending communications without a valid legal basis. What goes wrong: a marketing campaign uses customer data collected under a contract-performance basis, which does not authorize promotional messaging. Why it happens: the boundary between transactional and marketing communications is not clearly defined in the document generation system. How to prevent it: configure legal-basis rules at the template level so that each document type is tagged with its applicable basis and generates only for customers who meet the criteria.

4. Neglecting document accessibility. What goes wrong: PDF statements and contracts are generated without tags, logical reading order, or alternative text, making them inaccessible to assistive technologies. Why it happens: accessibility is treated as a "nice-to-have" add-on rather than a default output standard. How to prevent it: embed PDF/UA compliance in the template design and generation pipeline so every document is accessible by default.

5. Treating compliance as a one-time project. What goes wrong: a bank invests heavily in a compliance overhaul, then allows standards to erode as regulations change and staff turn over. Why it happens: compliance ownership is not clearly assigned, and monitoring tools are not in place. How to prevent it: assign regulatory monitoring responsibilities, implement automated compliance checks, and schedule at least quarterly reviews with additional reviews triggered by regulatory changes.

6. Inconsistent compliance across channels. What goes wrong: compliance rules are enforced for email communications but not for SMS or WhatsApp messages. Why it happens: each channel is managed by a different team with different tools. How to prevent it: use a centralized CCM platform that enforces uniform rules across all delivery channels.

7. Ignoring cross-border data transfer requirements. What goes wrong: customer documents containing personal data are processed or stored in jurisdictions without adequate data protection. Why it happens: cloud-based systems may route data through servers in multiple countries without explicit configuration. How to prevent it: configure data residency rules in the document pipeline and verify that all processing locations comply with applicable transfer requirements.

Multi-country complexity is the recurring root cause across all of these mistakes. Template drift, inconsistent local practices, and uneven tooling create compounding exposure that only centralized automation can reliably address.

Avoiding these mistakes starts with the right infrastructure. Talk to DocPath about building a compliance-first document workflow.

How Should Banks Handle Multichannel Compliance (Email, SMS, WhatsApp, Print)?

Each communication channel, including email, SMS, WhatsApp, print, and app notifications, brings distinct compliance obligations around consent, encryption, delivery confirmation, and retention. Banks must enforce channel-specific rules centrally while maintaining one unified audit trail.

The following table summarizes the primary compliance considerations for each channel:

|

Channel |

Consent Requirements |

Encryption/Security |

Delivery Confirmation |

Retention Obligations |

|

|

Consent or valid legal basis per document type |

TLS encryption in transit; encrypted storage recommended |

Read receipts, delivery status tracking |

Retain per regulatory schedule with full metadata |

|

SMS |

Explicit opt-in for marketing; legal basis for transactional |

End-to-end encryption not standard; content minimization critical |

Delivery receipt from carrier |

Retain message logs with timestamps |

|

|

Explicit opt-in required for business messaging |

End-to-end encryption by default |

Read receipts available through Business API |

Retain interaction logs; comply with WhatsApp Business Policy |

|

|

Generally does not require separate consent beyond the customer relationship |

Physical security of documents during production and mailing |

Tracked mail or registered delivery for regulated communications |

Retain generation records and proof of mailing |

|

App push/in-app |

Consent for push notifications; in-app may rely on contract basis |

App-level encryption; secure session management |

In-app read tracking; push delivery status |

Retain notification logs and interaction records |

WhatsApp is a particularly important channel in LATAM banking. In 2023, WhatsApp achieved more than 92% usage penetration among internet users in selected Latin American countries, making it the most used social network in the region. In Brazil alone, approximately 148 million people used WhatsApp in 2024, representing near-universal adoption among smartphone users. Banks operating in the region cannot ignore this channel, but must ensure that WhatsApp-based communications meet the same compliance standards as every other channel.

Centralized CCM is essential for consistent multichannel compliance. Without it, each channel operates under different rules, different tools, and different logging standards, creating gaps that regulators will identify during inspections. DocPath's multichannel delivery engine applies compliance rules, manages delivery orchestration, and maintains a unified audit trail across all channels. Banks that need real-time alerting capabilities across channels can also explore DocPath's Smart Alerts add-on.

How Do You Measure Compliance Effectiveness in Customer Communications?

Banks should track five KPIs to measure compliance effectiveness: template compliance rate, delivery confirmation rate, accessibility score, audit response time, and regulatory incident count. These metrics provide an objective, measurable view of how well compliance controls are performing.

|

KPI |

What It Measures |

Target Benchmark |

How to Track |

|

Template compliance rate |

Percentage of documents generated from current, approved templates |

100% (zero documents from outdated templates) |

Automated template version checks at generation time |

|

Delivery confirmation rate |

Percentage of communications with confirmed delivery across all channels |

Above 98% for digital channels; above 95% for print |

Channel-level delivery status tracking in CCM audit logs |

|

Accessibility score (PDF/UA pass rate) |

Percentage of generated documents that pass PDF/UA compliance checks |

100% for all customer-facing PDFs |

Automated accessibility validation integrated into the generation pipeline |

|

Audit response time |

Time required to produce a complete compliance record for a specific document or communication |

Under 24 hours |

Centralized audit log search and retrieval capabilities |

|

Regulatory incident count |

Number of compliance-related incidents, including fines, warnings, and customer complaints related to document compliance |

Zero; trending downward over time |

Incident tracking integrated with compliance monitoring dashboards |

Benchmarking should start with a baseline measurement of current performance across all five KPIs, followed by target-setting based on regulatory requirements and operational capacity. The role of production reporting and monitoring tools is critical here. DocPath's Sinclair monitoring tool provides real-time visibility into document generation volumes, delivery status, and system performance, supporting the continuous monitoring discipline that effective compliance requires.

Compliance Checklist: Before You Send That Customer Communication

Before sending any customer communication, banks should confirm legal basis, template approval, accessibility compliance, data minimization, channel authorization, and active audit logging, with each check mapped to the relevant regulatory category.

Use this checklist as a pre-send gate for every outbound customer communication:

- Legal basis confirmed. The applicable legal basis (consent, legal obligation, contract performance, or legitimate interest) has been identified and documented for this communication type. (Privacy)

- Template is current and approved. The template version has been reviewed, approved, and is current with the latest regulatory requirements for all applicable jurisdictions. (Consumer transparency)

- Data minimization applied. The communication contains only the personal data necessary for its stated purpose; no extraneous fields or identifiers are exposed. (Privacy)

- Accessibility standards met. The document output complies with PDF/UA standards, includes tagged content structures, alt text for images, and logical reading order. (Accessibility)

- Channel authorization verified. The customer has provided the required consent or opt-in for the specific delivery channel being used (email, SMS, WhatsApp, print, push notification). (Channel controls)

- Encryption and security controls active. Appropriate encryption is applied for the selected channel, and secure transmission protocols are in place. (Privacy / Audit/retention)

- Audit logging enabled. Generation, delivery, and acknowledgment events will be automatically logged with timestamps, document identifiers, and channel metadata. (Audit/retention)

- Retention rules configured. The communication and its metadata will be stored for the required retention period per applicable regulations. (Audit/retention)

- Breach notification readiness confirmed. If this communication involves sensitive data, the breach response plan is in place and notification templates are ready for the relevant jurisdictions. (Privacy)

- Regulatory review scheduled. The next review date for this template and communication type is set, with ownership clearly assigned. (Consumer transparency / Audit/retention)

Ready to automate compliance across every customer communication? Contact DocPath today to schedule a demo and see how our CCM platform keeps your banking documents compliant, accessible, and audit-ready.

Frequently Asked Questions

What is regulatory compliance in customer communications for banks?

Regulatory compliance in customer communications means every document a bank sends to customers, including statements, notices, contracts, and alerts, must meet data protection, consumer transparency, and accessibility standards set by operating jurisdictions. In Latin America, this includes laws such as Brazil's LGPD, Mexico's CNBV rules, and Colombia's Habeas Data Law.

Which Latin American countries have the strictest rules for banking communications?

Brazil and Mexico currently have the most comprehensive regulatory frameworks affecting banking customer communications. Brazil's LGPD imposes fines of up to 2% of revenue, capped at BRL 50 million per violation, and the Central Bank of Brazil has additional resolutions on cybersecurity and data handling. Mexico's CNBV requires detailed fraud prevention plans and individual transaction limits. Colombia, Chile, and Peru are also tightening requirements, particularly around customer authentication and data transparency.

How does LGPD affect the documents my bank sends to customers?

LGPD requires banks to have a valid legal basis, such as legitimate interest, legal obligation, or contract performance, before sending any customer communication. It also mandates data minimization in documents, gives customers the right to access and correct their data, and requires breach notification within three business days of confirming a qualifying incident. Banks must maintain records demonstrating compliance for all document processing activities.

Are accessible PDFs legally required for banks in Latin America?

Accessibility requirements are rapidly becoming legal obligations rather than optional best practices. The European Accessibility Act, enforceable since June 2025, mandates accessible digital documents for organizations operating in or serving European markets. Many LATAM banks with European operations or clients must comply. Additionally, ESG frameworks and emerging LATAM inclusion regulations are creating pressure for accessible communications. Since privacy laws like LGPD generally prohibit asking customers about disabilities, making all documents accessible by default is the safest compliance approach.

What is a CCM platform, and how does it help with banking compliance?

A Customer Communications Management (CCM) platform centralizes the design, generation, and delivery of customer-facing documents across all channels. For compliance, it enforces approved templates, automates data handling rules, generates accessible output formats, logs every document interaction for audit purposes, and applies jurisdiction-specific rules to multichannel delivery. This reduces manual error and ensures consistent compliance at scale.

How often should banks review their customer communication compliance?

Banks should review compliance at least quarterly, with additional reviews triggered by regulatory changes in any operating jurisdiction. In Latin America's fast-evolving regulatory landscape, continuous monitoring is more effective than periodic reviews. Automated monitoring tools within CCM platforms can flag template or rule changes in real time, supporting a proactive rather than reactive compliance posture.

Conclusion

Regulatory compliance in customer communications is not a one-off checkbox. In Latin America, it is a continuous, multi-jurisdiction discipline that demands automation, accessibility-first design, and centralized governance. This guide has covered the regulations that apply across six major LATAM markets, the compliance risks that banking document workflows face, the data privacy and accessibility requirements shaping document design, the step-by-step framework for building compliant processes, and the metrics that measure whether those processes are working.

The banks that manage this well are the ones that invest in CCM infrastructure capable of enforcing compliance and accessibility at the point of document generation, across every channel, without disrupting existing systems. DocPath provides that infrastructure, combining high-volume document generation, multichannel delivery, accessible PDF output, and audit-ready logging in a platform designed for multi-country banking operations. Contact DocPath to discuss how to bring your customer communications into full compliance.